.svg "Gorilla ROI")

Article Summary

🟤 Amazon FBM fee is not a single charge but a mix of fixed marketplace fees and variable fulfillment costs.

🟤 Shipping credits are standardized amounts that often differ from actual carrier invoices.

🟤 If your profit depends on shipping assumptions that are not actively monitored, your margin is more fragile than it appears.

Understanding Amazon FBM Fees

Most conversations about Amazon FBM fees focus on percentages.

Sellers compare referral rates, review shipping credits, and try to determine whether Fulfilled by Merchant is cheaper than FBA. On the surface, the math appears simple.

In practice, FBM profitability rarely deteriorates because someone misunderstood a referral percentage. It deteriorates because the cost structure was treated as fixed when it is inherently variable.

This article explains what sellers mean when they refer to an “Amazon FBM fee,” how FBM shipping rates interact with referral fees, and why margin stability depends on modeling sensitivity rather than memorizing fee tables. The objective is structural clarity, not a restatement of Amazon documentation.

What Sellers Mean by “Amazon FBM Fee”

There is no single line item labeled “Amazon FBM fee.” The phrase exists because sellers need shorthand for the full economic structure of Fulfilled by Merchant.

Under FBM, Amazon charges the same marketplace fees it charges any seller: a selling plan fee and a referral fee tied to category. What changes is that fulfillment responsibility moves onto your balance sheet. Shipping, packaging, labor, and operational variance are no longer absorbed inside Amazon’s logistics system. They become your variable cost.

Most miscalculations happen because sellers treat FBM as a fee comparison rather than as a cost structure. The marketplace commission is visible and stable. Fulfillment expense is variable and operationally sensitive. Margin durability depends on how those two layers interact.

The Marketplace Layer: What Amazon Actually Charges

The marketplace portion of FBM is predictable, and that predictability can create misplaced confidence.

Selling plan fees are fixed. Amazon referral fees are calculated as a percentage of total order revenue and vary by category. That percentage does not adjust when carrier rates increase, when dimensional weight classifications change, or when packaging decisions add incremental cost. Amazon’s commission remains constant regardless of your fulfillment exposure.

Because referral percentages are visible and easy to compare, they tend to dominate margin conversations. Fulfillment variability, which is distributed across carrier invoices, packaging decisions, and labor allocation, receives less attention. Under FBM, that imbalance in focus can distort pricing decisions.

Category shifts magnify this effect. Moving into a higher referral band reduces theoretical margin before shipping is even modeled. If the evaluation is performed at the revenue level rather than at effective take rate, contribution margin can be overstated from the outset.

The marketplace layer sets the ceiling. All fulfillment volatility operates beneath it.

The Fulfillment Layer: Where Margin Actually Moves

Under FBM, fulfillment is not operational background noise. It is the primary variable affecting profitability.

Amazon provides shipping credits based on order attributes and service level. These credits are standardized. Your actual shipping cost depends on dimensional weight, packaging, carrier contracts, and zone distribution. When those two systems diverge, the difference does not appear as a visible “Amazon fee.” It appears as a reduced net margin.

Dimensional weight often drives the divergence. A packaging modification, supplier change, or adjustment in box size can increase billable weight tiers even if the product itself remains unchanged. Unless those changes trigger a recalibration of pricing assumptions, margin compression can occur without obvious cause.

Labor and handling introduce further variability. Pick-and-pack time, error rates, reshipments, and service-level commitments all influence cost per order. These variables rarely change in a single dramatic shift. They move gradually, which makes them harder to detect at the aggregate level.

None of these factors are hidden; they are simply not centralized in one place unless the seller builds a consolidated cost model.

Shipping Credits Are Not Revenue

A common structural error in FBM modeling is classification.

Shipping credits appear alongside product revenue in reporting views, which makes it easy to treat them as income. In reality, they function as partial reimbursement against a variable carrier expense. They are not designed to match your actual invoice.

When shipping credits are absorbed into revenue assumptions, fulfillment efficiency appears stronger than it is. The discrepancy between standardized credit and real shipping cost may be small per order, but across volume it compounds, particularly when zone mix shifts or carrier surcharges change.

If shipping credits are modeled as reimbursement rather than revenue, margin sensitivity becomes visible. That distinction alone often changes how products are priced and evaluated.

When FBM Makes Economic Sense

FBM is neither inherently superior nor inherently riskier than FBA. Its durability depends on cost sensitivity.

FBM tends to perform more reliably when products have a strong price-to-weight ratio and when packaging and carrier selection remain consistent. In these scenarios, shipping expense remains within a predictable range relative to referral percentage.

It becomes less stable when products are bulky relative to price, when dimensional weight exposure is high, or when zone distribution fluctuates materially. In those cases, fulfillment expenses can shift independently of pricing while referral percentages remain fixed, narrowing the margin buffer.

The evaluation should be based on modeled sensitivity rather than headline fee comparison. If projected profit depends on best-case shipping assumptions, the structure is exposed. If moderate fluctuations do not materially reduce contribution margin, the model is more resilient.

How to Model Amazon FBM Fees Correctly

A defensible FBM model begins at the order level rather than at monthly aggregates.

Each order should incorporate product price, referral fee, selling plan allocation, shipping credit, actual carrier cost based on dimensional weight and zone, packaging materials, and fulfillment labor or 3PL expense. Averaging these inputs too early conceals margin sensitivity.

The objective is not perfect precision. It is awareness of exposure. If a modest increase in carrier cost materially reduces contribution margin, the product is structurally fragile under FBM. If typical volatility does not meaningfully alter profitability, the margin buffer is stronger.

Static assumptions applied to variable systems create optimism that does not hold under scale.

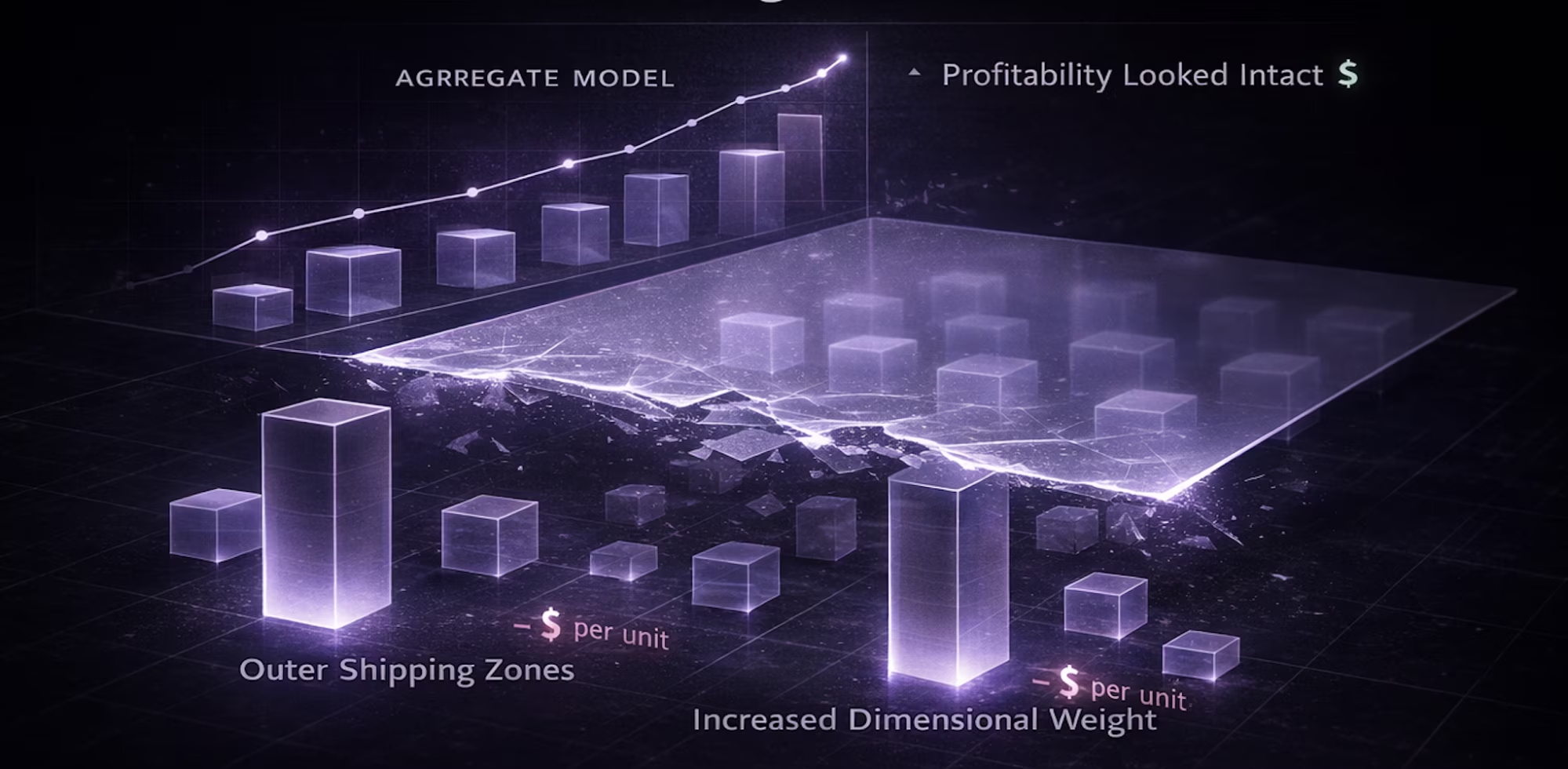

Case Study: When the Model Looked Right but Wasn’t

A mid-sized FBM seller in the home and kitchen category reported steady revenue and consistent referral fees, yet experienced gradual margin compression over several quarters. Advertising performance remained stable. Pricing had not changed significantly.

At the aggregate level, profitability appeared intact.

Order-level review revealed two incremental shifts. A higher percentage of orders were shipping to outer zones, increasing average carrier expense. At the same time, a packaging adjustment increased dimensional weight just enough to move shipments into a higher billable tier.

Neither shift was dramatic. Together, they reduced the contribution margin by several dollars per unit.

Referral fees had not changed, shipping credits remained consistent, and the model projected historical profitability because it relied on outdated averages rather than current exposure.

The correction required recalibrating dimensional weight assumptions, adjusting packaging, and updating the per-order cost model to reflect actual zone distribution.

The economics shifted quietly but the dashboard did not.

The Hidden Risk in FBM: Why “Stable” Margins Can Fail Without Warning

Most FBM instability does not begin with visible losses. It begins with averages that conceal exposure.

Orders remain profitable on paper. Shipping credits roughly align with historical invoices. Referral percentages are understood. What changes is the operating environment beneath those assumptions.

Advertising budgets and inventory purchasing decisions are based on expected contribution margin. When fulfillment expense rises gradually but pricing remains constant, the difference accumulates without an obvious signal.

The structural risk in FBM is not confusion about fees. It is the appearance of stability built on narrow operating assumptions.

Sellers who treat FBM as a simple fee comparison evaluate commission percentages. Sellers who treat it as a variable cost system model sensitivity and revisit assumptions regularly.

The difference determines whether margin compression is detected early or after scale.

FAQ: Amazon FBM Fees and Shipping Rates

What is an Amazon FBM fee?

There is no single “Amazon FBM fee.” The term refers to the combined effect of selling plan fees, Amazon referral fees, shipping credits, and the seller’s own shipping and fulfillment expenses under Fulfilled by Merchant.

How are Amazon referral fees calculated for FBM sellers?

Amazon referral fees are calculated as a percentage of total order revenue and vary by category. In many cases, the percentage applies to both product price and shipping charged to the customer.

Do FBM sellers keep the full shipping credit?

No. Shipping credits are standardized offsets. Actual FBM shipping rates depend on dimensional weight, packaging, carrier contracts, and zone distribution. The credit may not fully cover the real carrier invoice.

How do FBM shipping rates affect profitability?

FBM shipping rates are variable. Changes in dimensional weight, carrier surcharges, or zone mix can materially affect per-order margin even when referral percentages remain constant.

Is FBM cheaper than FBA?

FBM is not inherently cheaper than FBA. The outcome depends on product size-to-price ratio, fulfillment stability, and how well shipping cost sensitivity is monitored.

How should sellers calculate true Amazon FBM costs?

True Amazon FBM costs should be calculated at the order level, incorporating referral fees, selling plan allocation, shipping credits, actual carrier expense, packaging materials, and fulfillment labor. Monthly averages often obscure margin exposure.